Economy at a Glance - May 2023

Global Outlook Event

The International Monetary Fund (IMF) projects global growth to average 2.6 percent this year, down 0.6 percent points from ’22. That’s an improvement over projections made in the fall when the IMF forecast a tepid 2.2 percent this year.

Slower global growth will impact Houston’s economy but won’t lead to a local recession. The reasons why will be outlined at the Partnership’s State of Houston Global Economy luncheon, a comprehensive look at the region’s trade and investment ties. The event will be held Friday, May 12, at the Omni Hotel, and will feature a panel discussion among three executives whose firms are heavily involved in global trade:

- Laerte Barros, Head of International Subsidiaries Banking, Regions Bank

- Tom Heidt, Chief Operating Officer, Port of Houston Authority, and

- Takajiro Ishikawa, President & CEO, Mitsubishi Heavy Industries Americas, Inc.

George Y. Gonzalez, Partner with Haynes Boone, will moderate the discussion. Following the discussion, Patrick Jankowski, the Partnership’s chief economist, will present his forecast on the impact the global economy will have on the local economy this year. Attendees will also receive a copy of Global Houston, the Partnership’s analysis of the region’s ties to the world economy. To register for the event, visit the events page on the Partnership’s website.

U.S ECONOMIC OUTLOOK

U.S. economic growth has slowed considerably since January but the recession that so many predicted hasn’t arrived yet. It’s unlikely to knock on our doors before autumn, if at all. When it does, and if the recession is short and shallow, the impact on Houston will be minimal. Only if the U.S. slides into a deep and protracted downturn would Houston suffer.

A Closer Look at the Data

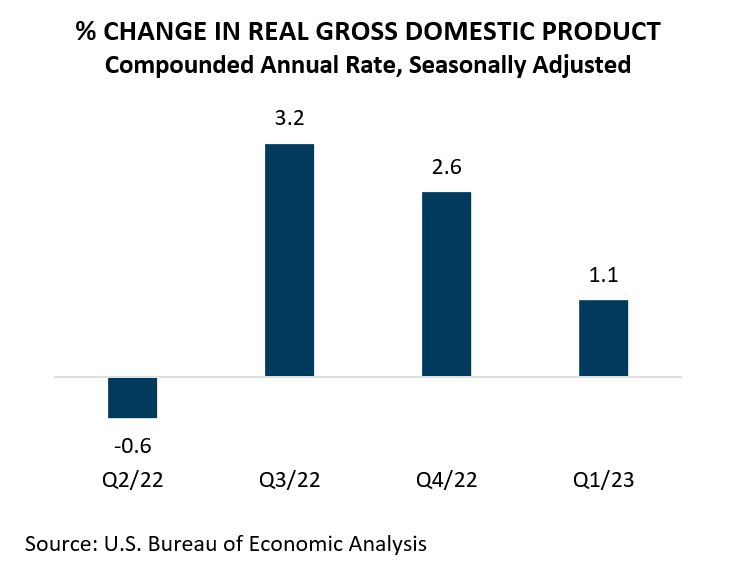

The Bureau of Economic Analysis (BEA) announced that gross domestic product (GDP) grew at a 1.1 percent annual rate in Q1/23, adjusting for inflation. This was well below the 30-year average of 2.5 percent. The media pointed to this as another sign of a slowing economy.

A closer look at what sapped Q1 GDP growth suggests the economy is stronger than the headline number indicates.

To calculate GDP, BEA looks at consumer spending across all sectors of the economy (haircuts, medical care, restaurant meals, travel, vehicles, home furnishings, etc.). Private investment comes into play. On the business side, this includes equipment, buildings, intellectual property, and inventories; on the consumer side, residential construction. BEA factors in federal, state, and local government spending. The final component is exports after imports have been subtracted.

Consumer spending, government spending, and net exports expanded in Q1, adding 3.5 percentage points to GDP growth. However, inventories and residential construction shrank, subtracting 2.4 percentage points from GDP growth. At some point, businesses will need to replenish those inventories. And housing, though still a mess, appears to be stabilizing. New home sales rose 9.1 percent in March, so inventory drawdowns and home construction will be less of a drag on future growth.

A Lack of Consensus

Despite the headlines, the economics community isn’t unified in the belief that a recession is imminent. In March, the Nation Association for Business Economics (NABE) asked its members about the likelihood of a recession in the next 12 months. Forty-nine percent placed the probability at less than 50 percent. Only 44 percent of the respondents place the probability at 50 percent or more. In its most recent survey, The Wall Street Journal found one-fourth of their respondents placed the probability of a recession in the next 12 months at less than 50 percent.

So why the worry? Several reasons.

The Federal Reserve has embarked on a series of interest rate hikes nine times since ’61 to rein in inflation. Eight times, a recession followed. Inflation remains high, so the Fed will likely raise rates this month and in June. Economists worry the Fed will raise rates too high and hold them there for so long that the Fed crashes the economy, not just slow it down.

The manufacturing sector has contracted for five consecutive months, according to the Institute for Supply Management. Historically, seven consecutive declines have aligned with the U.S. economy slipping into recession.

In March, Conference Board’s Leading Economic Index fell to its lowest level since November ’20. The Expectations Index, which is based on consumers’ near-term outlook for income, business, and labor market conditions, has tracked below 80, the level associated with a recession within the next year, 14 of the past 15 months.

The nation’s banks continue to tighten lending standards. In its Q1 Senior Loan Officer Opinion Survey on Bank Lending Practices, the Fed found that 44.8 percent of respondents had tightened lending standards for large and middle market firms, 43.8 for small firms, 28.3 percent for credit card loans, and 17.3 percent for auto loans. Tightening of credit has preceded three of the last four recessions.

The yield curve inverted last March and has remained there since. Inverted yield curves have preceded the past six recessions. The curve inverts when short-term and long-term interest rates flipflop. Investors are more worried about the economic outlook over the next few months than over the next few years, so they demand a risk premium (i.e., interest rates) for their short-term investments versus their long-term investments.

Not There Yet

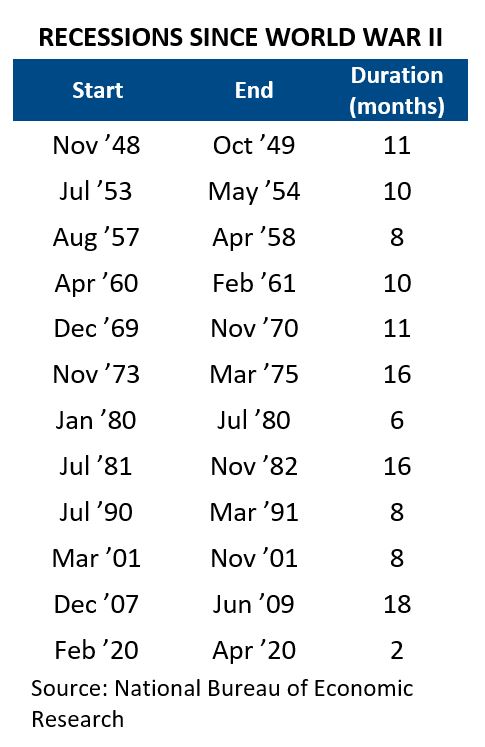

But the U.S. has not slipped into a recession. Most of the indicators that the National Bureau for Economic Research (NBER) tracks to determine the peaks and troughs of the business cycle show the economy still expanding.

- The nation created jobs, 236,000 in March and 1.0 million since the first of the year, according to the BLS.

- A different employment indicator, one based on a survey of households, shows the nation added 577,000 jobs in March.

- Though industrial production began to slide in September, a slow recovery began in January and continued into March.

- Personal income continues to grow, even after adjusting for inflation, though growth has tapered in recent months.

- Personal consumption expenditures are holding steady.

- Only manufacturing and wholesale show signs of weakness in the data NBER tracks.

Headlines warning that the U.S. is barreling toward a recession first appeared in March ‘22, soon after the Fed announced its initial interest rate hike. The media, policymakers, and economists have been beating that drum ever since.

Eventually, the U.S. will slip into a recession. Contractions are a normal part of the business cycle, just as sunshine and rain are normal for Houston’s weather.

Although the outlook for the economy remains cloudy, the Partnership sees no rain in the near-term forecast. But it would wise to keep an umbrella nearby, just in case.

To continue reading, download this report.

Note: The geographic area referred to in this publication as “Houston,” "Houston Area” and “Metro Houston” is the nine-county Census designated metropolitan statistical area of Houston-The Woodlands-Sugar Land, TX. The nine counties are: Austin, Brazoria, Chambers, Fort Bend, Galveston, Harris, Liberty, Montgomery and Waller.